Predatory lenders target people with bad credit or no credit history because they know those borrowers have fewer options. Knowing the warning signs of predatory lenders before you apply for any loan can save you hundreds of dollars and serious stress.

These eight signs appear again and again in loan scams and in products that may be technically legal but are designed to trap you in debt. Read them once and they’ll stick with you.

A predatory lender is one that uses deceptive, manipulative, or outright illegal tactics to get you into a loan you can’t afford or don’t understand. The goal is not to help you borrow money. It’s to collect fees.

Predatory lending shows up in several forms: fake lenders that steal your personal information, legitimate-looking lenders with buried fees, and aggressive marketers pushing products with triple-digit APRs and no real repayment path. The damage is real. The Consumer Financial Protection Bureau tracks tens of thousands of loan-related complaints each year.

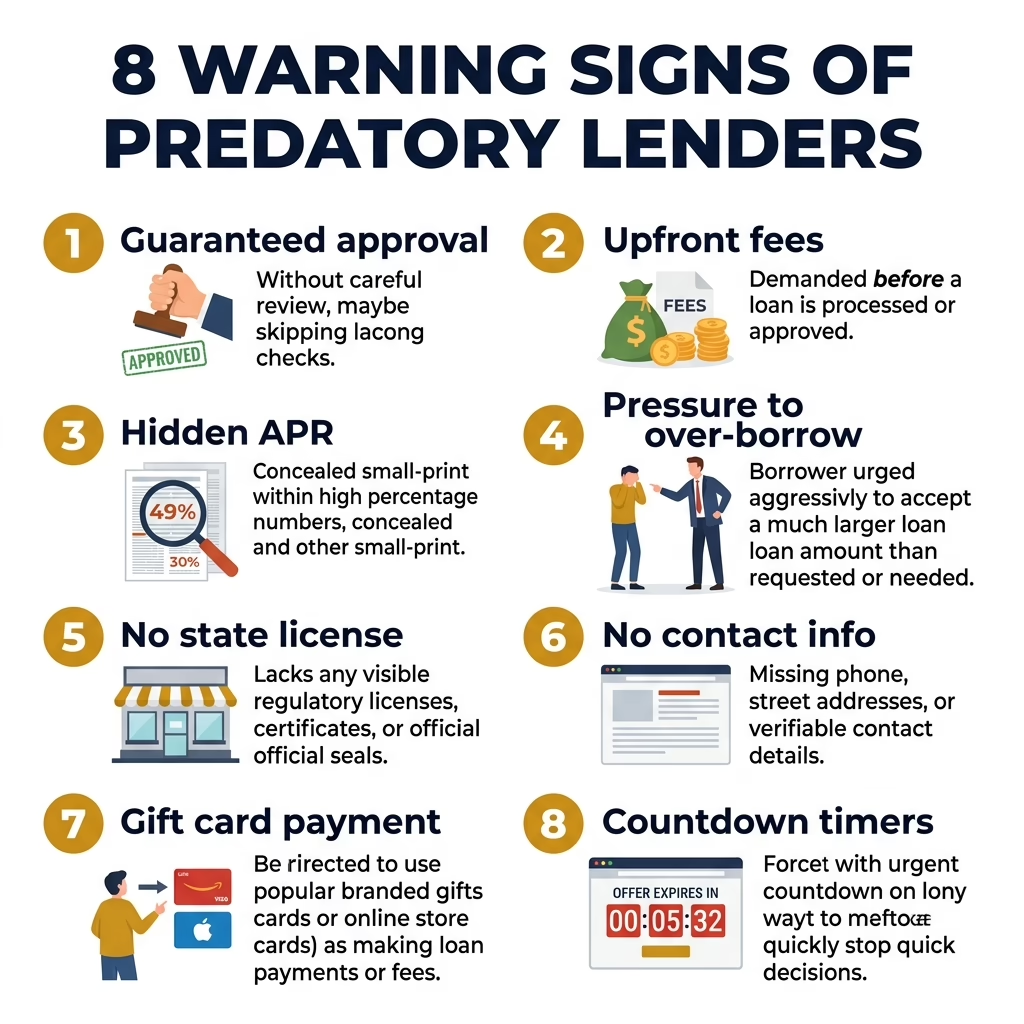

No legitimate lender can guarantee you a loan before reviewing your application. They need to check at minimum your income, your state of residence, and sometimes your banking history. A “guaranteed approval” claim is either false advertising or a setup for a bait-and-switch where the terms change after you submit personal data.

Real lenders do not charge you before giving you money. If someone asks for an “insurance fee,” “processing fee,” or “security deposit” before your loan is funded, stop. This is the most common loan scam pattern. Once you send that money, it’s gone.

Under the Truth in Lending Act, lenders must disclose your APR, total loan cost, and payment schedule before you sign. If a lender won’t give you these numbers up front, walk away. You should never have to accept a loan to find out what it costs.

If you ask for $300 and the lender keeps pushing $1,500, that’s a red flag. Larger loans mean larger fees. A lender whose job is to help you will match the loan to what you actually need.

Yes, in most cases. Advance-fee loan fraud is illegal under federal law and state laws in Texas, Missouri, and Utah. If a lender demands payment before you receive funds, report them to your state financial regulator and the FTC.

Lenders in Texas, Missouri, and Utah must hold a state license to legally make personal loans. An unlicensed lender cannot enforce the loan terms in court and has no accountability to state regulators. Always verify a lender’s license before applying.

A real lender has a physical address, a working phone number, and a customer service team you can actually reach. If the only contact option is a web form or a generic email address, that’s a problem. Run a search for the company name plus “complaint” or “scam” before going further.

No legitimate financial company asks for payment via gift card or wire transfer. These methods are irreversible, which is exactly why scammers prefer them. Legitimate lenders collect payments via ACH bank transfer or check.

“Act now or lose your rate.” “This offer expires in 10 minutes.” Urgency tactics are designed to stop you from thinking clearly. Real loan offers do not disappear in an hour. If a lender is rushing you, slow down.

The fastest check is the NMLS Consumer Access registry. Type the lender’s name and confirm they hold an active license in your state. This takes about 60 seconds and eliminates most scam operations.

Also check the Better Business Bureau profile, look for a physical address on Google Maps, and call their customer service line before submitting any personal information. Legitimate lenders expect you to do your homework.

Before applying anywhere, search “lender name + complaint” or “lender name + scam” in Google. If there are dozens of recent complaints, move on.

Each state has a financial regulator where you can verify lender licenses and file complaints:

The FTC received over 2.4 million fraud reports in a recent year. Imposter scams, including fake loan companies, were the top category. Texas consistently ranks in the top five states for fraud reports.

A high-interest lender charges more than a bank but operates legally and transparently. A predatory lender uses deception, hidden fees, or illegal tactics regardless of the interest rate. You can have a high-rate loan that is not predatory if the terms are fully disclosed before you sign.

Yes. A license means the lender has met state registration requirements, not that their practices are ethical. Some licensed lenders use aggressive rollover terms, confusing contracts, and high-pressure sales tactics. Always read the full agreement.

Stop all contact with the lender. Do not send any more money. File a report with your state regulator, the FTC at reportfraud.ftc.gov, and the CFPB at consumerfinance.gov/complaint. If you shared bank information, contact your bank immediately.

Loan Ridge works with a network of licensed lenders operating in Texas, Missouri, and Utah. Every lender in our network must comply with applicable state and federal lending laws.

Loan Ridge connects borrowers in Texas, Missouri, and Utah with licensed lenders. Check your options with no impact to your credit score. See if you qualify for a personal loan.

Written by

Consumer-finance writer

Daniel has 12 years of experience in consumer lending and personal finance. Daniel focuses on transparency in lending and helping borrowers understand the true cost of the products they sign for.